Sorry, no sales person is available right now to take your call. Pls leave a message and we will reply to you via email as soon as possible.

Home/ PCB News/ Dual-Track Resonance: New Energy Vehicles and AI Computing Power Reshape the Ceramic Substrate Industry Landscape

Dual-Track Resonance: New Energy Vehicles and AI Computing Power Reshape the Ceramic Substrate Industry Landscape

2026-07-15

I. Industry Overview: From Behind-the-Scenes Supporting Role to Core Industrial Component

Ceramic substrates are not a new material. Thanks to their excellent electrical insulation, ultra-high thermal conductivity, and stable mechanical support properties, they have long served as a critical foundational carrier for power semiconductors and precision electronic devices, widely used in industrial power supplies, rail transit, photovoltaic inverters, LED lighting, lasers, optical communications, and high-reliability semiconductor packaging.

Currently, the industry is entering a clearly defined high-growth cycle, primarily driven by the simultaneous boom in two high-momentum sectors: new energy vehicles (NEVs) and AI computing data centers. Technological iteration and large-scale deployment in these sectors have significantly elevated the essential demand for high-end ceramic substrates, shifting them from an “invisible” behind-the-scenes component to center stage in the electronics industry’s upgrade trajectory.

II. Market Size: A Billion-Dollar Golden Track with Markedly Divergent Segment Growth

2.1 Overall Market: Clear High-Growth Trajectory

Different institutions use varying statistical scopes (some counting only substrate products, others covering the entire component value chain), yet all consistently affirm the industry’s sustained high growth. The market has now entered a billion-yuan growth phase:

| Data Source | Market Size in 2025 | Long-Term Forecast | CAGR |

|---|---|---|---|

| Hengzhou Chengsi | Approx. RMB 12.88 billion | Exceeding RMB 32.07 billion by 2032 | 14.0% (2026–2032) |

| THS / Industry Institutions | Approx. RMB 3.29 billion | RMB 18–20 billion by 2026 | 18.69% |

2.2 Segment Breakdown: Structural Opportunities Show Significant Divergence

Different subcategories serve distinct application scenarios, resulting in markedly differentiated growth rates—premium, high-precision segments are growing far faster than the industry average:

AMB Ceramic Substrates: Global sales reached approximately USD 586 million in 2025 and are projected to grow to USD 1.832 billion by 2032. Among these, high-end silicon nitride (Si₃N₄) AMB substrates are experiencing the most rapid growth—global market size stood at USD 143 million in 2025, with a CAGR of 23.47% from 2025 to 2032, making it the key incremental category for automotive-grade applications.

HTCC Ceramic Substrates: The market is growing steadily, with global sales expected to reach RMB 22.6 billion by 2026 and a CAGR of 7.8% from 2026 to 2032, primarily serving high-reliability, high-temperature industrial and military applications.

Optical Module Ceramic Components: Benefiting from the rapid iteration of AI-driven high-speed optical modules, this segment is experiencing explosive growth. The market size is projected to reach RMB 13.5 billion in 2026 (RMB 9.9 billion for substrates and RMB 3.2 billion for housings) and could climb to RMB 20–22 billion by 2027, with a short-term CAGR exceeding 60%, positioning it as a core beneficiary of AI computing demand.

III. Competitive Landscape: Overseas Dominance in High-End Segments, Domestic Substitution Enters Critical Window

3.1 Global Landscape: Clear Tier Structure, High Concentration

The global ceramic substrate industry currently exhibits a stable structure: “Japan leads in high-end, Europe and the U.S. focus on mid-range, and China is catching up.” Market concentration is notably high:

Upstream Base Materials: Japanese companies Denka, MARUWA, and Kyocera firmly occupy the top tier globally, monopolizing core powder and sintering technologies for high-thermal-conductivity aluminum nitride and silicon nitride substrates, creating formidable barriers.

Midstream Metallized Substrates: Overseas firms such as Rogers and Ferrotec set global benchmarks, dominating the premium precision substrate market.

Market Concentration: The top five global manufacturers collectively hold approximately 59% market share. The high-end segment remains under long-term overseas monopoly, while domestic players primarily focus on mid-to-low-end applications.

3.2 Critical Window for Domestic Substitution: Dual Drivers of Policy and Low Penetration

China’s high-end ceramic substrate industry is encountering a historic substitution opportunity, propelled by two key catalysts:

Policy-Driven Supply Chain Restructuring: Yttrium oxide—a critical raw material for aluminum nitride substrates—has been included in China’s rare earth export controls, directly constraining Japan’s capacity to produce high-end aluminum nitride powder. This disrupts the long-standing overseas-dominated supply chain and creates market space for domestic technological breakthroughs and capacity substitution.

Extremely Low High-End Penetration, Vast Substitution Potential: Domestic localization rate for high-end aluminum nitride powder is only around 4%, with core raw materials and premium precision substrates heavily reliant on imports—offering enormous potential for both replacement of existing imports and expansion into new demand.

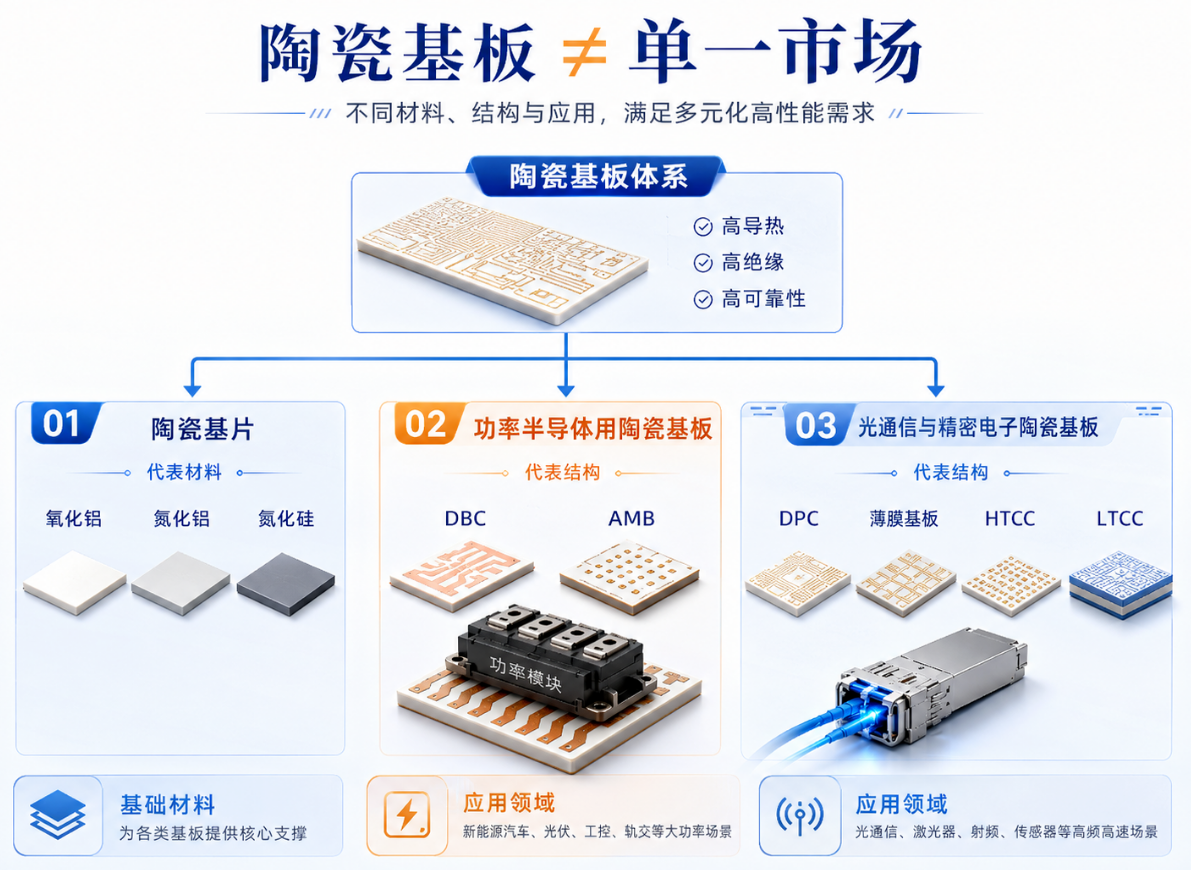

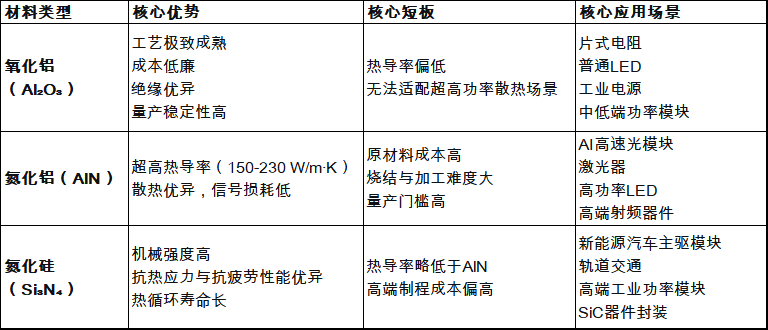

IV. Three Material Pathways: Differentiated Applications, Long-Term Coexistence and Complementarity

Alumina, aluminum nitride, and silicon nitride represent three distinct technological pathways with no absolute substitution relationship. Leveraging differentiated performance, cost, and reliability profiles, they precisely match diverse downstream needs and will coexist long-term:

V. Dual Downstream Engines: NEVs and AI Computing Mutually Empowering Growth

5.1 New Energy Vehicles: Structural Growth Driver for Silicon Nitride AMB Substrates

New energy vehicles represent the most critical growth engine for high-end silicon nitride AMB substrates, driven fundamentally by comprehensive technological upgrades in onboard power modules:

800V high-voltage platforms are accelerating adoption, imposing stringent requirements on substrate voltage tolerance, heat dissipation, and long-term reliability;

Silicon carbide (SiC) devices are progressively replacing traditional silicon-based components, significantly increasing power density and heat generation;

Conventional substrates struggle to meet the complex operating conditions of vehicles, whereas silicon nitride AMB substrates offer thermal cycling lifespans exceeding 500,000 cycles—10x higher than traditional DBC substrates—making them an essential solution for automotive-grade power modules.

Structurally, silicon nitride accounts for 96% of automotive AMB substrates, establishing absolute dominance. The global Si₃N₄ AMB substrate market is projected to reach USD 818 million in 2026 and grow to USD 2.297 billion by 2033, with a CAGR of 15.89% from 2026 to 2033.

5.2 AI Data Centers: A New Growth Curve for Aluminum Nitride Precision Substrates

AI computing demand for ceramic substrates is not centered on GPU body cooling but rather on three key areas: high-speed optical modules, precision optoelectronic packaging, and high-end server boards—opening entirely new growth avenues for aluminum nitride substrates:

High-Speed Optical Module Iteration: Deployment of 800G, 1.6T, and 3.2T optical modules intensifies challenges in heat dissipation and signal loss under high-frequency, high-speed conditions. Aluminum nitride ceramic substrates can maintain optoelectronic chip junction temperatures below 60°C, offering over 5x better thermal performance than conventional substrates and reducing signal transmission loss by 40% compared to FR-4, making them a core precision material.

AI Server Board Upgrades: Next-generation Rubin GPUs may reach peak power consumption of 2,850W, forcing material innovation in server boards. Ceramic substrates have already replaced nearly 30% of traditional PCBs in AI server boards, with further substitution potential ahead.

CPO (Co-Packaged Optics) Technology Evolution: CPO integrates optical engines and switch chips in close proximity, causing localized heat spikes. This places extreme demands on substrate flatness, dimensional accuracy, thermal expansion matching, and heat dissipation—further driving essential demand for high-end aluminum nitride substrates.

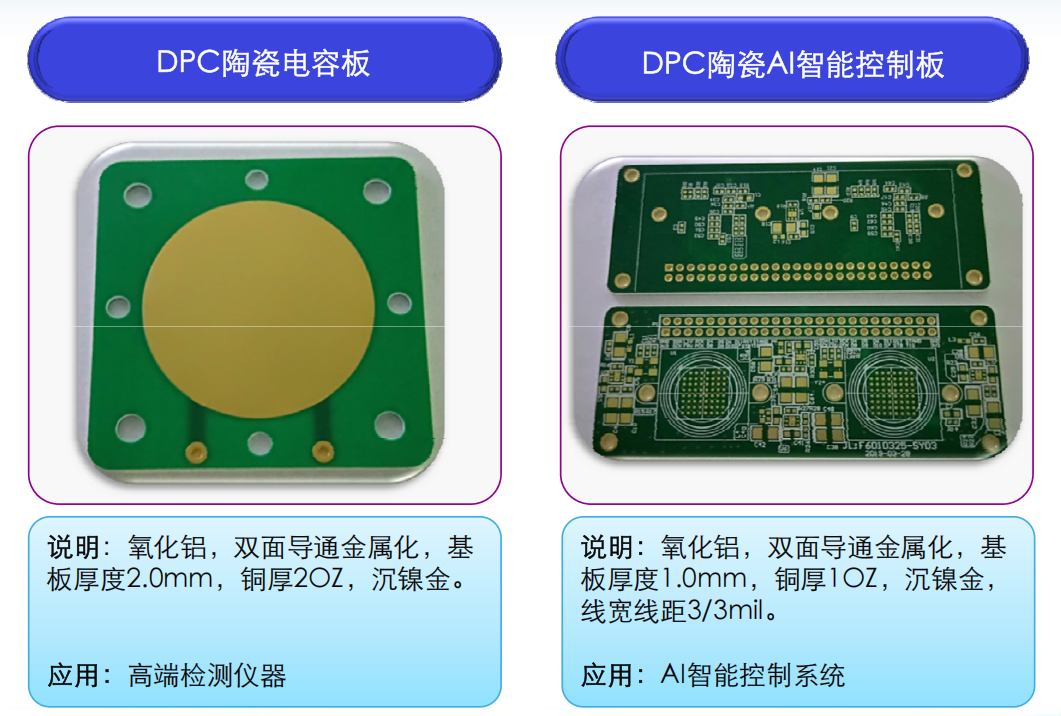

VI. Benchmark Company: BN-Yunban – A Domestic Pioneer with Full-Category Coverage

BN-Yunban is a rare domestic manufacturer offering full-process, full-category ceramic substrates. It masters six core fabrication technologies, serving consumer, industrial, automotive, and computing applications, and is among the few Chinese companies achieving large-scale production of high-end ceramic substrates—standing out as a benchmark in domestic substitution.

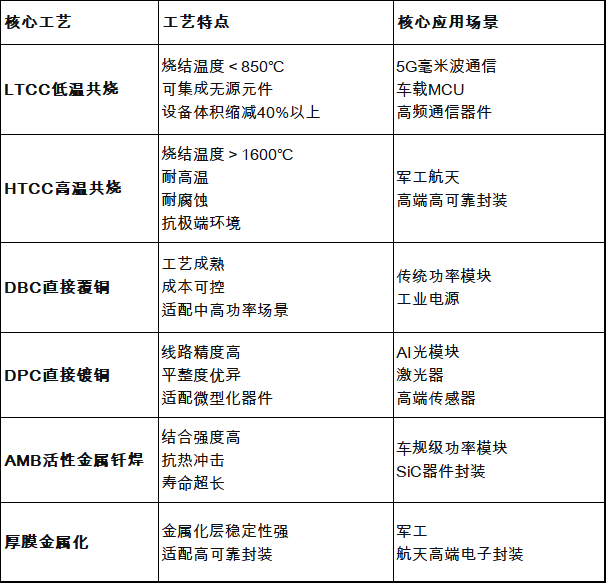

6.1 Six Core Processes, Comprehensive Multi-Scenario Coverage

6.2 Core Product Capabilities

Premium Thermal Management: Aluminum nitride substrates consistently achieve thermal conductivity of 150–230 W/m·K, reducing junction temperatures of high-power devices by 15–25°C—perfectly suited for AI computing and automotive high-power thermal demands.

Automotive Certification: Products pass 1,000 thermal shock cycles between -40°C and 125°C and 2,000-hour salt spray reliability tests, fully compliant with IATF 16949 automotive standards, qualifying for mass vehicle OEM supply.

High Integration & Lightweighting: LTCC technology embeds 12 thick-film resistors (±1% tolerance) and 8 multilayer capacitors, shrinking traditional MCU module volume from 50 cm³ to 30 cm³—enabling miniaturization and integration upgrades.

6.3 Differentiated Competitive Advantages

Unlike competitors focused on single processes or product lines, BN-Yunban’s core strength lies in its integrated solution capability combining “ceramic substrates + PCB hybrid integration.” The company deeply engages in early-stage customer thermal design and structural development, offering end-to-end services—from material selection and substrate process optimization to multilayer circuit design, reliability testing, and mass production—creating deep, hard-to-replicate ecosystem advantages with high-end downstream clients.

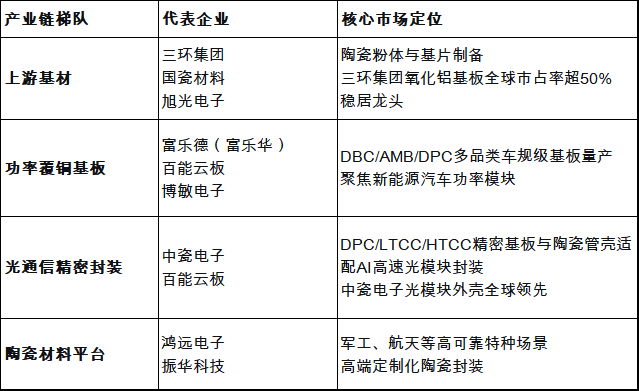

VII. Tiered Overview of Key Domestic Players Across the Value Chain

Domestic core enterprises can be categorized into four tiers based on their position in the value chain and technological focus:

VIII. Industry Risks and Core Challenges

Statistical Scope Discrepancies: Definitions and coverage of the ceramic substrate industry vary across institutions; cross-study comparisons require careful validation to avoid misjudgment.

Insufficient Domestic High-End Material Localization: Core high-end raw materials remain monopolized overseas; domestic localization rate for premium aluminum nitride powder is only ~4%, creating bottlenecks due to weak upstream supply chain autonomy.

High Full-Chain Technical Barriers: High-end ceramic substrates involve multiple core technologies—powder sintering, interface bonding, stress control, and precision machining—making consistent, stable mass production extremely challenging and prolonging entry timelines for newcomers.

Highly Divergent Sub-Segments: Alumina, silicon nitride, and aluminum nitride belong to entirely distinct markets with different technical paths, customer bases, pricing logics, and valuation frameworks—requiring precise, granular analysis.

Concept Hype Risk: High industry interest has led some companies—possessing only pilot lines or technical reserves without scalable production or delivery capabilities—to ride the trend. Rigorous differentiation between genuine leaders and speculative shell entities is essential.

The growth narrative of the ceramic substrate industry is clear: dual-sector structural upgrades are converging—NEV high-voltage systems and SiC localization are expanding demand for high-reliability silicon nitride AMB power substrates, while AI computing speed and packaging precision are accelerating iteration of aluminum nitride optical communication substrates. The industry has evolved from a traditional industrial support material into a critical, essential base material for the two core sectors of NEVs and AI.

Amid the wave of domestic substitution, BN-Yunban—backed by full coverage of six core processes, automotive-grade mass production capability, and its unique “ceramic + PCB” integrated advantage—has strategically positioned itself in the two high-momentum tracks of automotive power and AI optical communications, emerging as China’s rare full-category, high-end ceramic substrate leader. However, investors must remain vigilant about significant segment divergence, formidable technical barriers, and upstream “chokepoint” risks. Future industry analysis and investment should focus on companies with proven technology, real mass production, and verified delivery capabilities, carefully distinguishing growth logic and profitability cycles across different product categories.

BN-Yunban Ceramic Substrate Product Showcase

trending news

Contact Us